Blackarbs Retirement Strategy Algorithm Debut (Part 1)

/

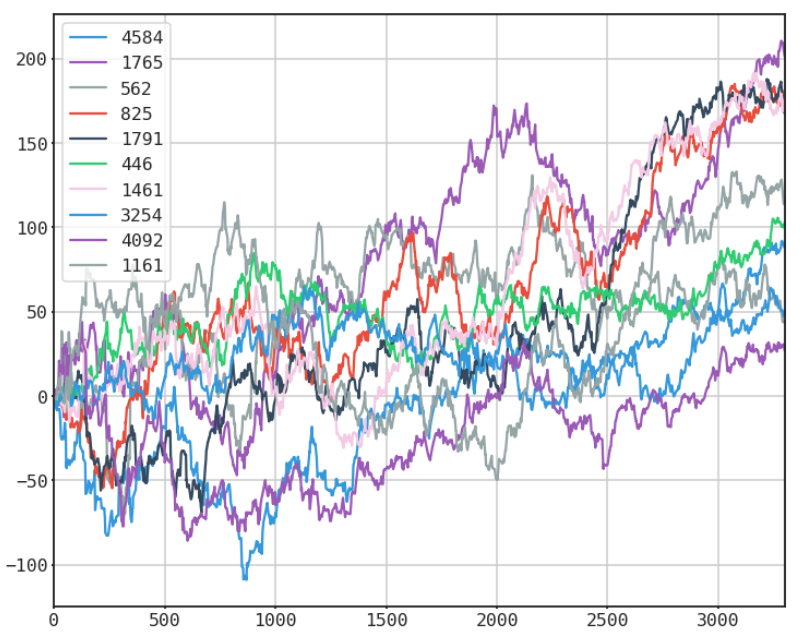

Blackarbs current mission is to create automated strategies with the goal of beating the market with superior risk adjusted returns. Originally, I wanted to illuminate some of the more hidden aspects of markets and investing that I found interesting and of value. Over time, that goal crystallized into creating a strategy or strategies that made (potential) superior performance accessible to investors of all types and demographics. To this end I believe we have finally created a flagship algorithm.

Read More